Why this firm matters

At $609.3B pre-move market value, ExxonMobil Corp. is among the largest firms in the cohort and carries disproportionate weight in market-value-weighted aggregates.

Controller & ownership

Diffuse / non-controlledOwnership concentration data not yet documented for this firm.

Source: Widely held, no controlling shareholder

Vote outcome — reincorporation proposal

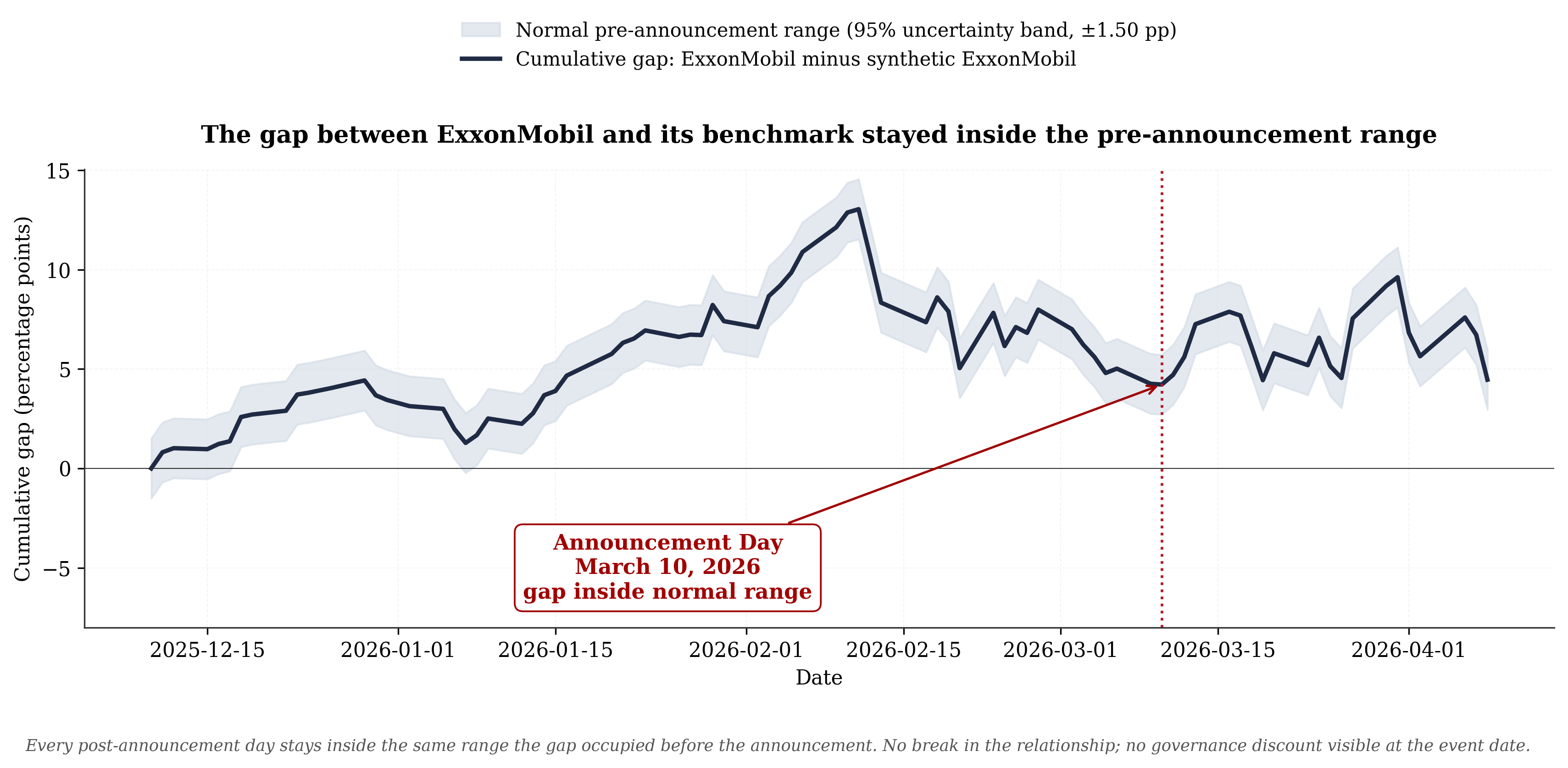

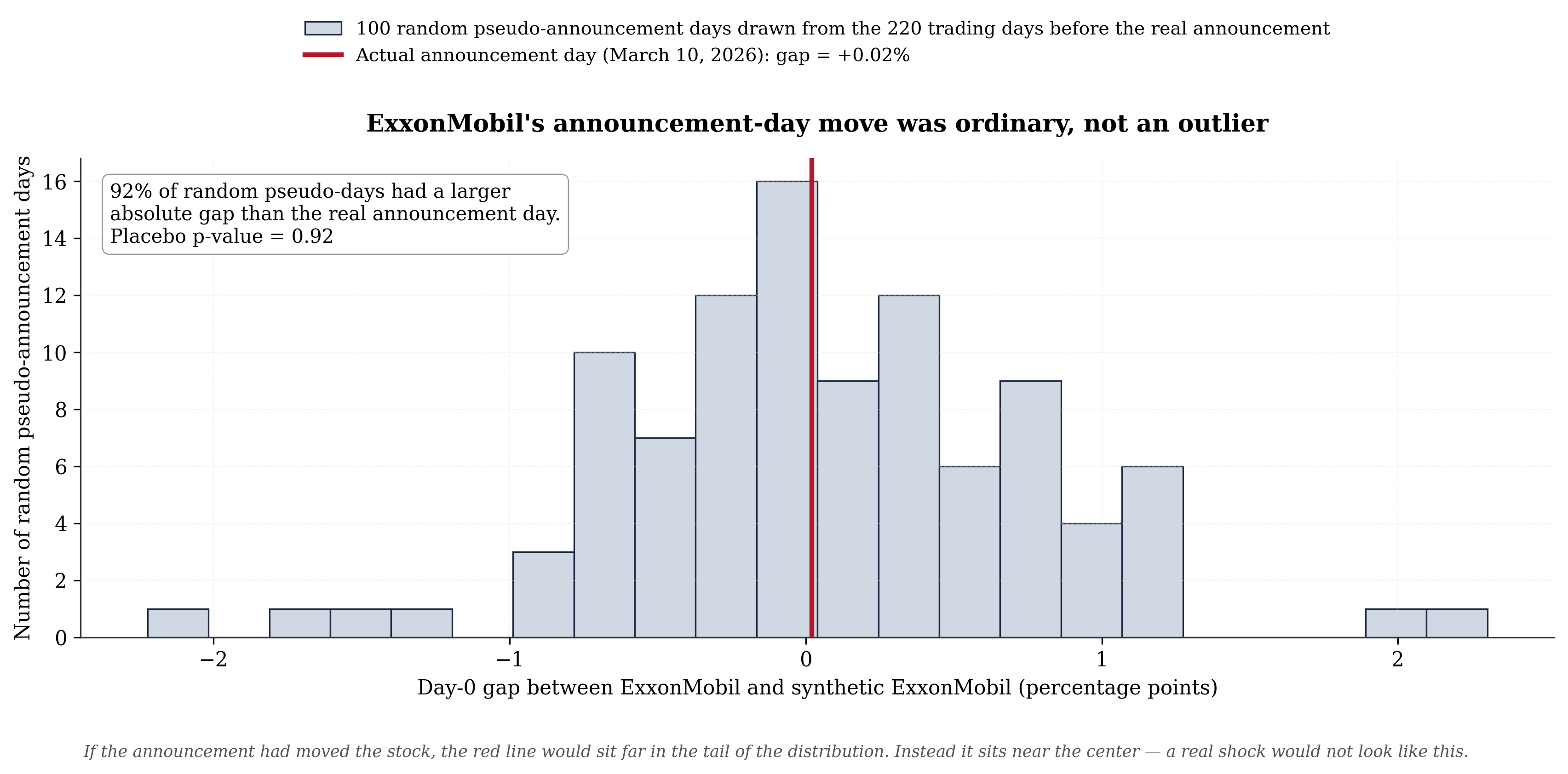

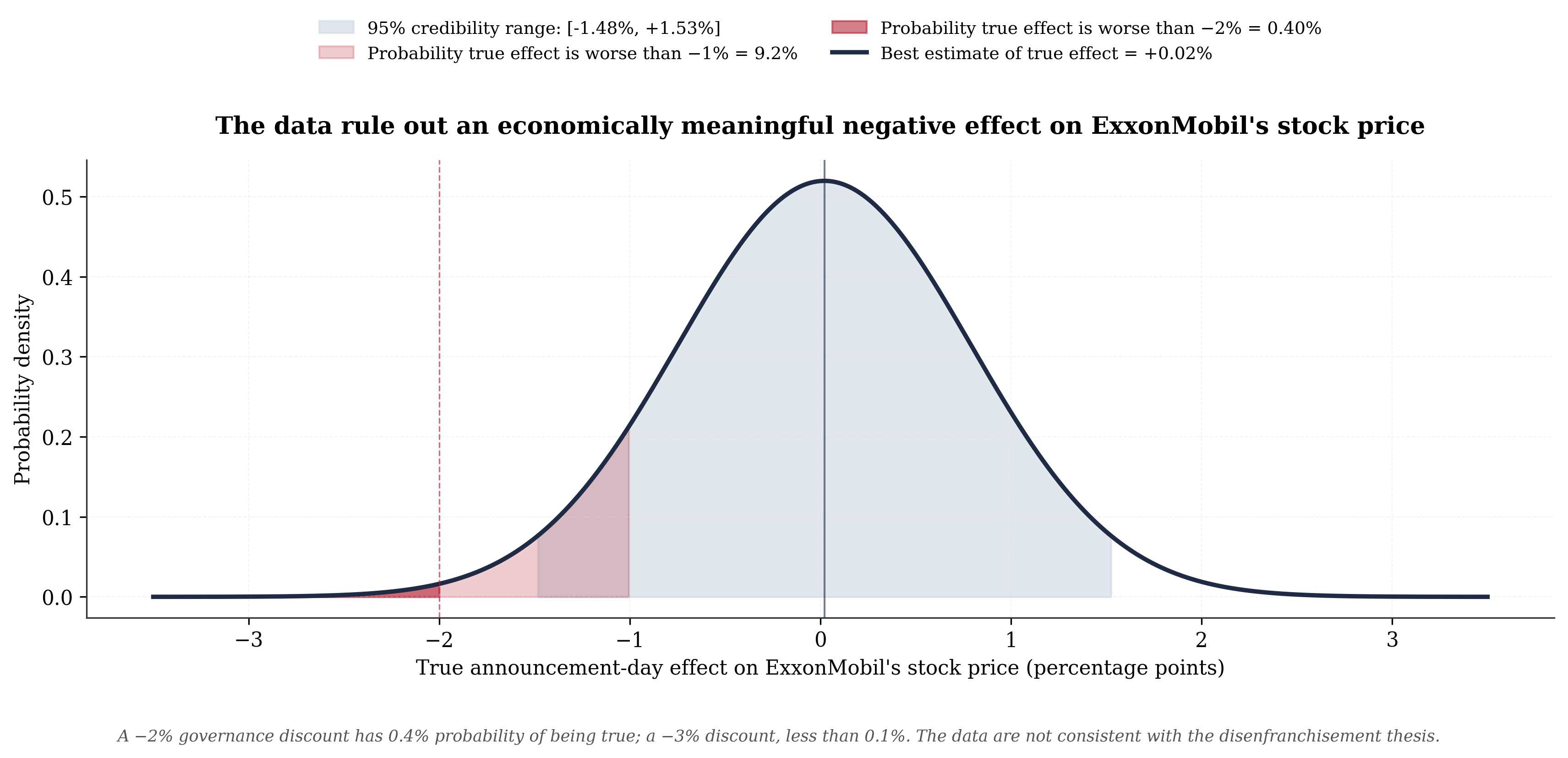

Visual evidence — event study around the March 10, 2026 announcement

xom_rerun_results.json (estimation window 2025-03-25 to 2026-03-09, 240 trading days; 21 energy-sector donors; SC top-3 weights CVX 0.55, EOG 0.20, SLB 0.09).

xom_rerun_results.json in the replication kit. Open methodology and underlying code → Event-study abnormal returns — announcement window

| Specification | Day-0 AR | Inference |

|---|---|---|

| Synthetic control (21-donor energy peer pool)i | -0.11% | placebo p-value (in-time, gap-based) = 0.955 |

| Market model (SPY benchmark)i | -1.55% | Patell-z p-value = 0.281 |

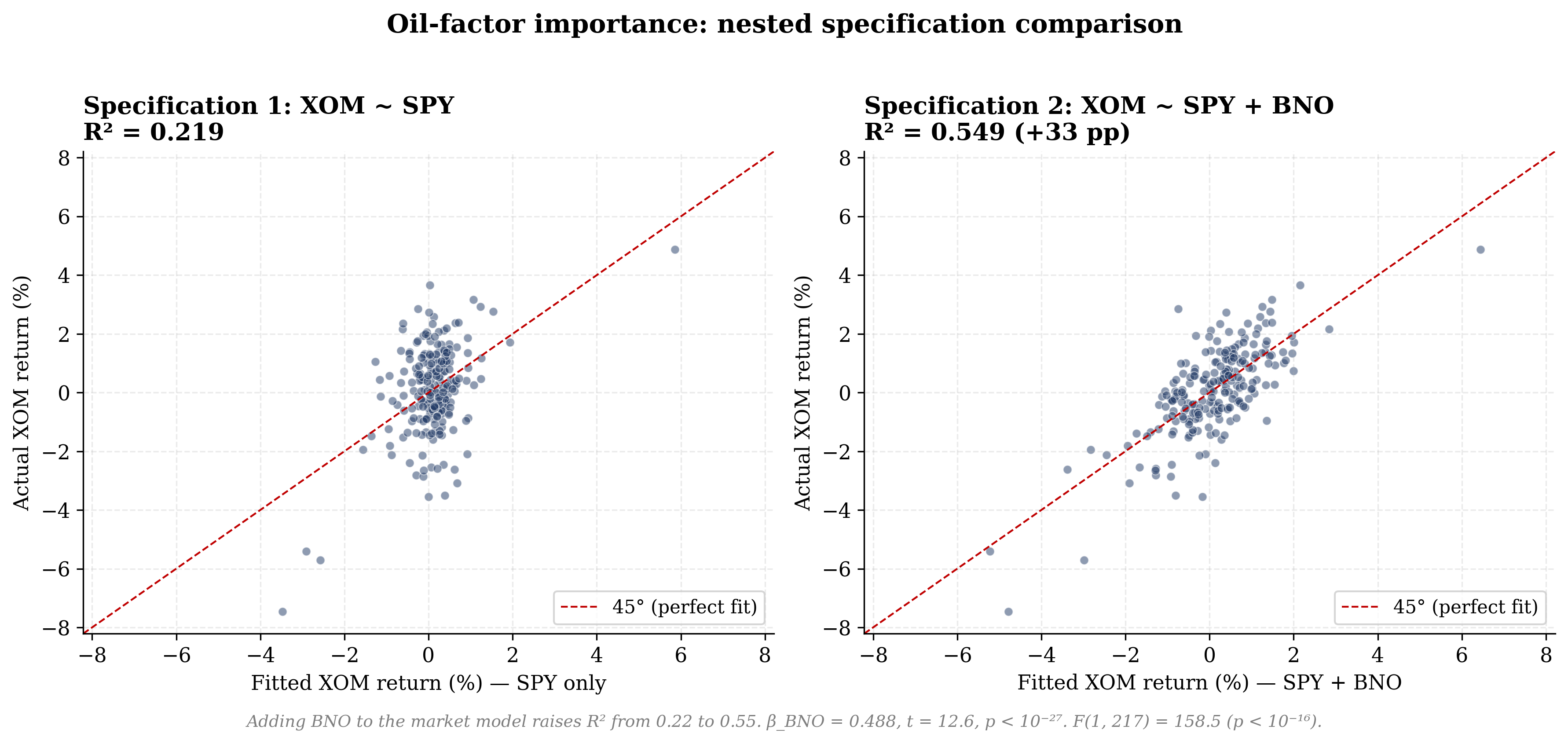

| Oil-augmented market model (SPY + WTI) HEADLINEi | -2.19% *** | Patell-z p-value = 0.049 |

| Matched pair vs CVX (market-model-adjusted)i | +0.04% | two-sided p-value = 0.958 |

| Raw differential vs CVXi | +0.13% | no inference |

Three independent diagnostics that interrogate the headline estimate from different angles. All three pointing the same way = high confidence in the result.

- Pre-event drift check: the firm's daily abnormal return drifted by -0.0002% per day in the pre-event window (p = 0.820). no detectable pre-event drift ✓. — A near-zero slope means the pre-event period was stable, so the day-0 reaction is not contamination from a pre-existing trend.

- Donor co-movement check: 10 of 11 peer firms moved in the same direction as the treated firm on the event day (binomial p = 0.0117). — A high concordance means the day was driven by industry-wide news rather than something firm-specific. A low concordance means the firm moved differently from peers (potential firm-specific signal).

- Synthetic-control fit quality: pre-event correlation between the firm and its synthetic twin = 0.886 (good tracking); R² = 0.771 (fraction of pre-event variance explained); Durbin-Watson = 1.88 (no autocorrelation). — Higher correlation + higher R² + Durbin-Watson near 2 means the synthetic peer was a good match before the event, so the post-event gap is interpretable.

Event-study abnormal returns — vote window

Vote window CARs not yet computed (vote on 2026-05-27).

Long-run abnormal returns & pooled estimates

No long-run / pooled estimates available for this firm yet — run phase5z_compute_longrun.py on Windows to populate (requires effective date ≥ 3 months ago).

Cohort-level robustness battery

Heckman two-step selection correction (controlled-vs-widely-held)

Cohort ATE = +0.94% (SE = 7.06%, n = 2395) after correcting for controller-status selection (inverse Mills ratio = -0.062).

Romano-Wolf step-down + Benjamini-Hochberg FDR (n = 47)

This firm: raw p = 0.282, Romano-Wolf adjusted p = 1.000, BH-FDR adjusted p = 0.966. Multiple-hypothesis correction is computed across the full cohort to control family-wise error rate at alpha = 0.05.

Pooled cohort BHAR (mover firms only)

BHAR_63d: mean = -5.60% (SE = 22.11%, n = 3, p = 0.499) · BHAR_126d: mean = +17.33% (SE = 41.17%, n = 3, p = 0.774)

See Cohort event study → for the full battery and forest plots.

Texas Statutory Adoptions

The Texas opt-in statutory regimes (TBOC §21.552 / SB 29 derivative threshold; TBOC §21.373 / SB 1057 shareholder-proposal threshold) are available only to firms that are nationally listed Texas corporations. ExxonMobil Corp. is not yet Texas-incorporated; the move is pending shareholder vote with a proposed effective date of 2026-05-27. These adoptions can be elected only on or after the firm's TX effective date.

Source filings

- IR — https://investor.exxonmobil.com/

- EDGAR — https://www.sec.gov/cgi-bin/browse-edgar?action=getcompany&CIK=0000034088&type=&dateb=&owner=include&count=40

- Proxy — https://www.sec.gov/cgi-bin/browse-edgar?action=getcompany&CIK=0000034088&type=DEF+14A&dateb=&owner=include&count=40

- PRE 14A ·

0001193125-26-098908— filing → - Note. PRE 14A 0001193125-26-098908 (filed 2026-03-10); DEF 14A 0001193125-26-147614 (filed 2026-04-08); DEFA14A response filings 2026-05-12 (Glass Lewis) + 2026-05-15 (ISS)

Classification & audit trail

Related firms

← Back to The Reincorporation Tracker · Cohort event study · JSON for XOM